Regulatory Consolidation

By Steve Gens | July 2023

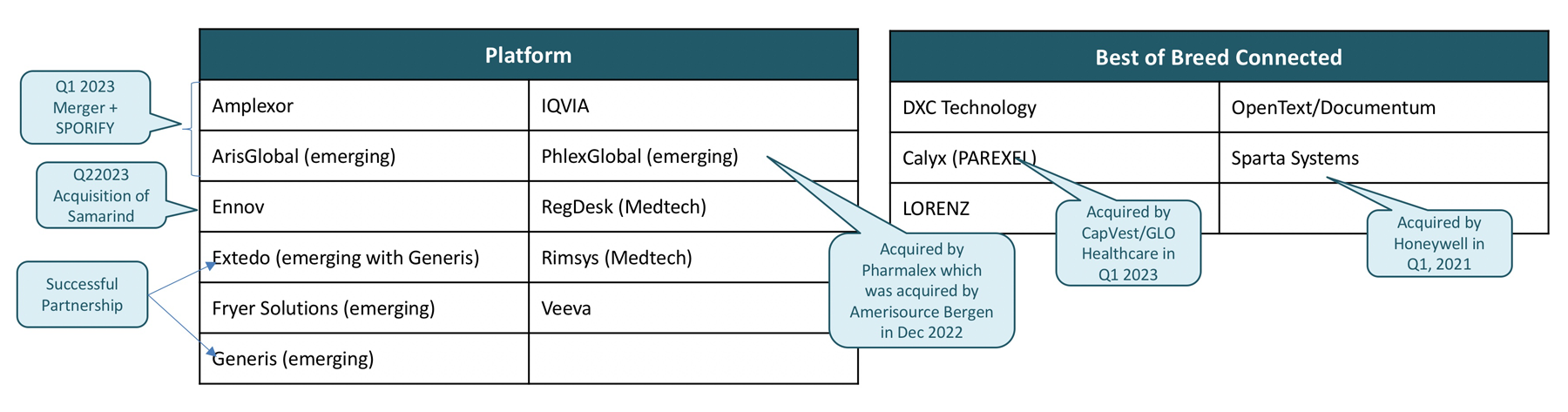

It’s been an interesting 12 months to say the least with ArisGlobal buying both Amplexor and SPORIFY, Ennov buying Samarind, Calyx divestiture from PARAEXEL only to be acquired by CapVest/GLO Healthcare in Q1 2023, and Honeywell buying Sparta Systems. We also witnessed some successful partnerships, especially the combined Generis/Extedo capabilities in both systems and services.

So, what does this all mean and why this pace of “consolidation”? Simply put, it’s the result of 7 + years of significant system and process modernization (relaying the regulatory foundation) where “end to end” thinking, Cloud/SaaS adoption, data quality & connectivity, and simplification were the driving forces.

The regulatory system landscape has greatly changed during these years resulting in many providers shifting their position in these different system strategy categories:

I recently discussed this topic with industry veteran John Cogan via a 20-minute information packed podcast moderated by Katherine Yang-Iott (Regulatory Software Provider Consolidation Impact with Steve Gens and John Cogan).

Here are five key insights that I believe you will find interesting:

Finally, our public World Class RIM study whitepapers provide a deeper analysis of these points while our membership have access to our comprehensive and detailed regulatory software and services market reports that are updated several times a year.